2022. 11. 6. 10:30ㆍEconomics

Overview

11월 FOMC가 한국 시간으로 11/2일 새벽에 열렸다. 시장의 예상대로 0.75% 자이언트 스텝을 밟았지만, 파월의 예상보다 매파적인 발언들에 주식 시장은 화들짝 놀란 모습을 보여주었다. FOMC 내용과는 별개로 현재 거시 경제 상황을 보면 생각보다 좋지 않은 상황들이 지속되고 있다. 지난 한 달 다소 완화된 모습을 보여주긴 했지만 여전히 강달러가 지속되고 있으며, 러 - 우 전쟁은 아직 끝날 기미를 보이지 않아 국방비 지출과 공급망 이슈, 그리고 원자재 문제에 대한 우려를 키우고 있다. 전쟁과 별개로 반도체 규제를 통해 드러난 심화된 미-중 갈등과 일대일로 사업으로 빚을 진 3세계 국가들의 연이은 디폴트 선언, 미국의 생각대로 움직여줄 생각이 없는 사우디를 포함한 OPEC 국가들의 석유 가격 통제등은 경제를 코로나 이전 상황으로 돌리기 위해 꽤나 많은 실타래들을 풀어야 함을 암시하는 듯하다.

FOMC Transcript

My colleagues and I are strongly committed to bringing inflation back down to our 2 percent goal. We have both the tools that we need and the resolve it will take to restore price stability on behalf of American families and businesses. Price stability is the responsibility of the Federal Reserve and serves as the bedrock of our economy. Without price stability, the economy does not work for anyone

연준의 가장 중요한 목표는 이러나저러나 인플레이션을 2%대로 낮추는 것이다. 가격 안정성 없이는 어떤 경제 시스템도 제대로 동작할 수 없다고 판단한 것이다.

Today, the FOMC raised our policy interest rate by 75 basis points, and we continue to anticipate that ongoing increases will be appropriate

이에 따라 인플레이션을 잡기 위해 지난 FOMC에 이어 0.75%의 기준 금리 인상을 하고, 추가적인 인상이 적절할 것으로 보인다고 언급했다. 여기서 "추가적인 인상"이라는 것은 다음 12월 FOMC에서도 기준 금리를 인상하겠다는 내용이 아니라 시장이 기대하고 있는 수준, 즉 11월 0.75bp 인상 후 4%가 된 기준 금리에서 12월에 0.5% 인상 후 23년 3월 0.25% 인상하는 것 이상으로 금리를 올리는 것이 적절해 보인다는 것이다. 이는 내년 3월 이후 미국의 기준금리가 5% 이상이 될 수 있다는 것을 의미한다. 시장은 금리 인하까지는 아니더라도 이번 0.75% 인상 이후 금리 인상 속도를 늦춰주거나 추가적인 인상을 다시 고려해보는 것을 기대했던 것 같지만 기대 이상의 금리 인상에, 이러한 금리가 생각보다 길게 지속될 수 있다는 발언에 화들짝 놀랐다.

Despite the slowdown in growth, the labor market remains extremely tight,

Although job vacancies have moved below their highs and the pace of job gains has slowed from earlier in the year, the labor market continues to be out of balance, with demand substantially exceeding the supply of available workers

연준이 지속적으로 금리를 올리겠다고 판단한 주요 기준 중의 하나는 "여전히 탄탄한 고용시장"이다. 고용시장의 불균형은 연초의 정점(peak)에서는 내려왔지만, 여전히 수요를 공급이 따라가지 못하는 상황이다.

FOMC Q & A

아래는 FOMC 연설 후 기자회견에서 파월이 답변한 내용을 정리한 것이다.

We think there's some ground to cover but before we meet that test and that's why we say that ongoing rate increases will be appropriate, and as I mentioned, incoming data between the meetings, both a strong labor market report but particularly the CPI report, do suggest to me that we may ultimately move to higher levels than we thought at the time of the September meeting

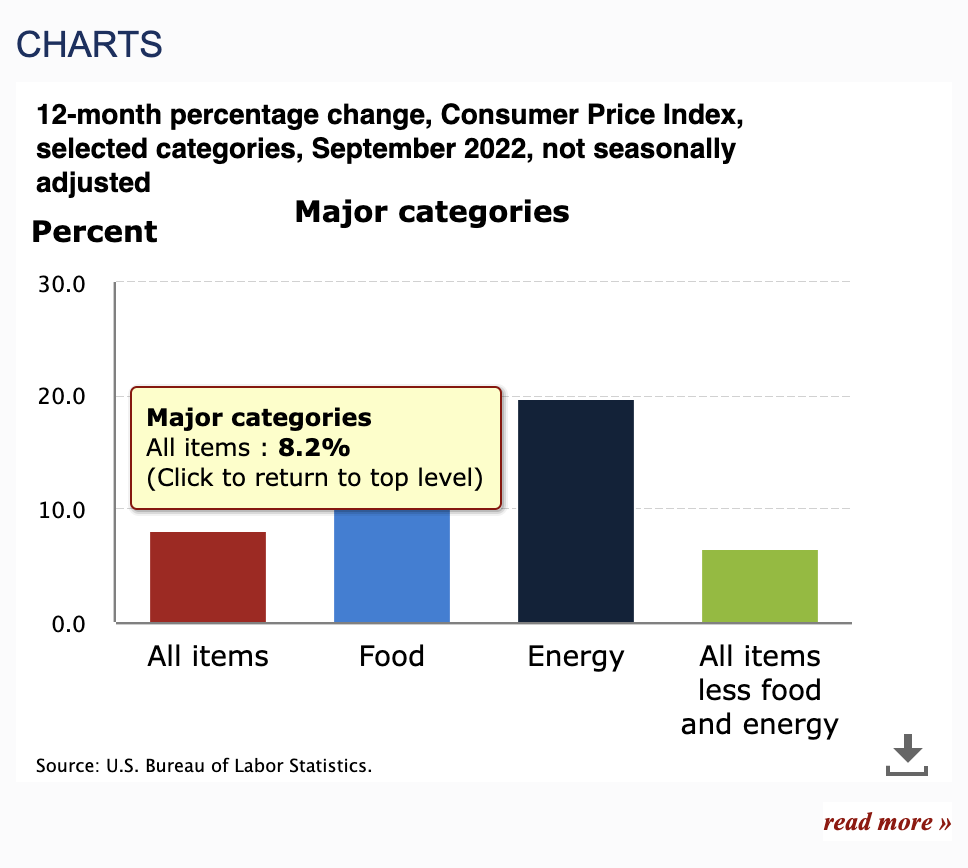

9월에 생각했던 것보다 높은 수준의 금리 인상을 고려하게 된 이유는 고용 시장은 여전히 탄탄한데 비해, CPI 지수는 여전히 높은 수준(8.2%)을 보여주고 있기 때문이다.

To be clear, let me say again, the question of when to moderate the pace of increases is now much less important than the question of how high to raise rates and how long to keep monetary policy restricted, which really will be our principal focus.

"금리 인상 속도를 조절하는 것"은 연준에게 최우선 순위는 아니며, 얼마나 높이 올릴 것인가와 얼마나 오래 유지할 것인가가 더 중요하다.

So, I think it's a very difficult place to be but I would tend to be, want to be in the middle looking carefully at what's actually happening with the economy. And trying to make good decisions from a risk management standpoint, remembering of course that if we were to over-tighten, we could then use our tools strongly to support the economy, whereas if we don't get inflation under control because we don't tighten enough, now we're in a situation where inflation will become entrenched and the costs, the employment costs in particular, will be much higher potentially. So, from a risk management standpoint, we want to be sure that we don't make the mistake of either failing to tighten enough, or loosening policy too soon.

연준은 70년대 Stop & Go로 섣부르게 금리 인상 속도를 조절했다가 낭패를 본 경험을 기억하고 있다. 따라서 차라리 "과도하게 긴축하는"것이 낫고, "과소한 긴축으로 인해서 인플레이션을 막지 못하는 상황"은 만들지 않겠다고 이야기한다. 과도한 긴축은 연준이 나중에 "loosening"해서 경기를 부양하는 데 사용할 수 있지만, 과소한 긴축으로 인해 인플레이션이 재발하게 된다면 이를 해결하기 위해서 상당히 오랜 기간 동안 고생해야 하므로, 차라리 과도한 긴축을 선택하겠다는 뜻으로 풀이된다.

'Economics' 카테고리의 다른 글

| [Essay] More than meets the eye (12월 FOMC Review) (0) | 2022.12.18 |

|---|---|

| [Essay] After Like (0) | 2022.11.27 |

| [Essay] broken pieces (0) | 2022.10.09 |

| [Essay] Not Yet (9월 FOMC Review) (0) | 2022.10.02 |

| [Essay] Don't fight the Fed (0) | 2022.09.18 |